Vermont’s Lake Champlain Cleanup Plan, Explained

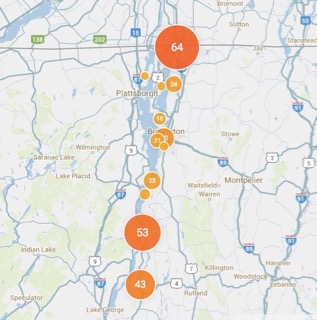

435 square miles of lake, 630 metric tons of phosphorus and one controversial plan to clean it up.

435 square miles of lake, 630 metric tons of phosphorus and one controversial plan to clean it up.

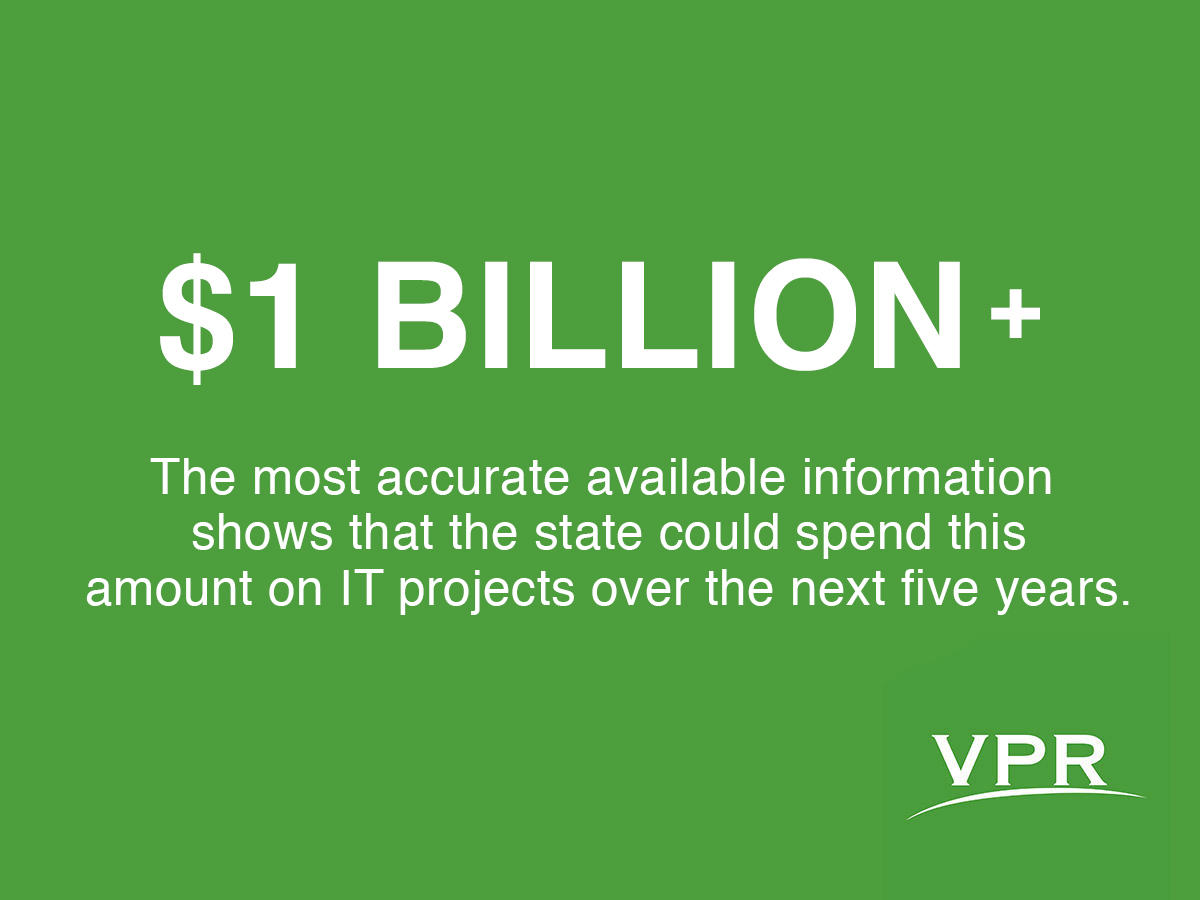

The state of Vermont doesn’t track what it spends on information technology, so we did it ourselves.

With health care reform, charges for supplies become untethered from costs. (Vermont Business Magazine)

As the Vermont Legislature works to overcome a $100 million budget gap for fiscal year 2016, one of its largest fiscal liabilities remains outside the reach of the annual budget bill. The state gives up about $1 billion in tax breaks annually through policies that have remained largely unchanged in recent years, even as lawmakers struggle to balance budgets.

Unlike state spending, most of the tax breaks are permanent – unless they’re amended. They’re not voted up or down annually like the budget. But every two years, the state tallies how much money it’s not collecting. Here’s the latest glimpse of who gets to keep it.

On Aug. 28, 2011, Tropical Storm Irene began flooding state employees out of their Waterbury offices and psychiatric patients out of their beds.

Three years later, steel beams three stories tall with cross bars at the top prop up faded brick walls from a courtyard. A mason from Irasburg fills ground-level windows with oversized granite bricks. A Monarch butterfly rests on a swaying stalk of tall grass that sprouted next to an oak tree circled in chain link fence.

Investors cry foul after Jay Peak owner converts their $500,000 equity stakes into unsecured IOUs.

1348 words / VTDigger.org

If IBM were to sell its computer chip-making unit to California-based Globalfoundries — patents and all, as the company is widely rumored to be considering — would the new owner of Vermont’s largest manufacturing plant even want to keep it?

Probably not, according to Len Jelinek, a semiconductor manufacturing industry analyst for the global information firm IHS.

IBM is Vermont’s largest private employer, with about 4,000 workers, and anxiety about the impact of the plant’s sale and potential closure is palpable.

Despite these feverish efforts to keep IBM in the Green Mountain State, there is little the state can do to prevent a potential closure of the plant. Global trends are driving behind-the-scenes negotiations between powerful industry players.

Job losses of IBM’s magnitude are easier to absorb over time, economist Art Woof acknowledged. Still, he said, the area’s financial engine is diversified and resilient enough that even such a “worst case scenario” would not kill the economy.

3332 words / VTDigger.org

Ariel Quiros is the entrepreneurial force behind Jay Peak ski resort and the $600 million Northeast Kingdom Economic Development Initiative – one of the largest development projects ever attempted in Vermont.

Though the project is high profile, Quiros is not. The international tycoon, though sometimes seen, is seldom heard.

The first generation American stands out at press conferences for his mystique: When he’s not got the ear of the governor, Quiros is most often seen standing uncomfortably before a crowd with pursed lips, staring silently and expressionless, at nothing in particular, through ice blue eyes.

Quiros quietly presides over an integrated set of projects that together constitute the largest private investment Vermont has ever seen: expansions at Jay Peak, development of the newly renamed Q Burke Mountain ski area, the mixed use Renaissance Block planned for downtown Newport, the future site of a biotech firm in the same town, and the promise of a new and improved Newport State Airport in Coventry.

“I make the vision,” he says quietly, a touch of gravel in his voice after 20-plus years of smoking.

3310 words / VTDigger.org

It’s the day before Q Burke Mountain opens for the winter, and Ary Quiros could just as well be preparing for battle as for business.

The new CEO is opening the ski resort for the first time since he started at the mountain the previous winter, and he’s amped. If Quiros, 36, can turn this chronically failing but beloved ski area into a stable business, he will succeed where prior, much wealthier, owners have failed.

The arc of history and local expectations give him long odds. But Quiros — and his staff — are determined.

Wearing a weathered, Army green jacket and frequently checking a watch face practically the size of his wrist, Quiros shuttles from one outpost of operations to another to check on his troops: snowmaking, ticket sales, kitchen, pub and cafeteria. Finances. Marketing. Housecleaning.

“It’s like being in the Army again,” Quiros says.

801 words / VTDigger.org

Statewide base property tax rates might increase again — by a nickel in 2015 — to meet the rising cost of education. But in recommending the rate bump, Tax Commissioner Mary Peterson also suggests looking for a way to get schools to curb spending.