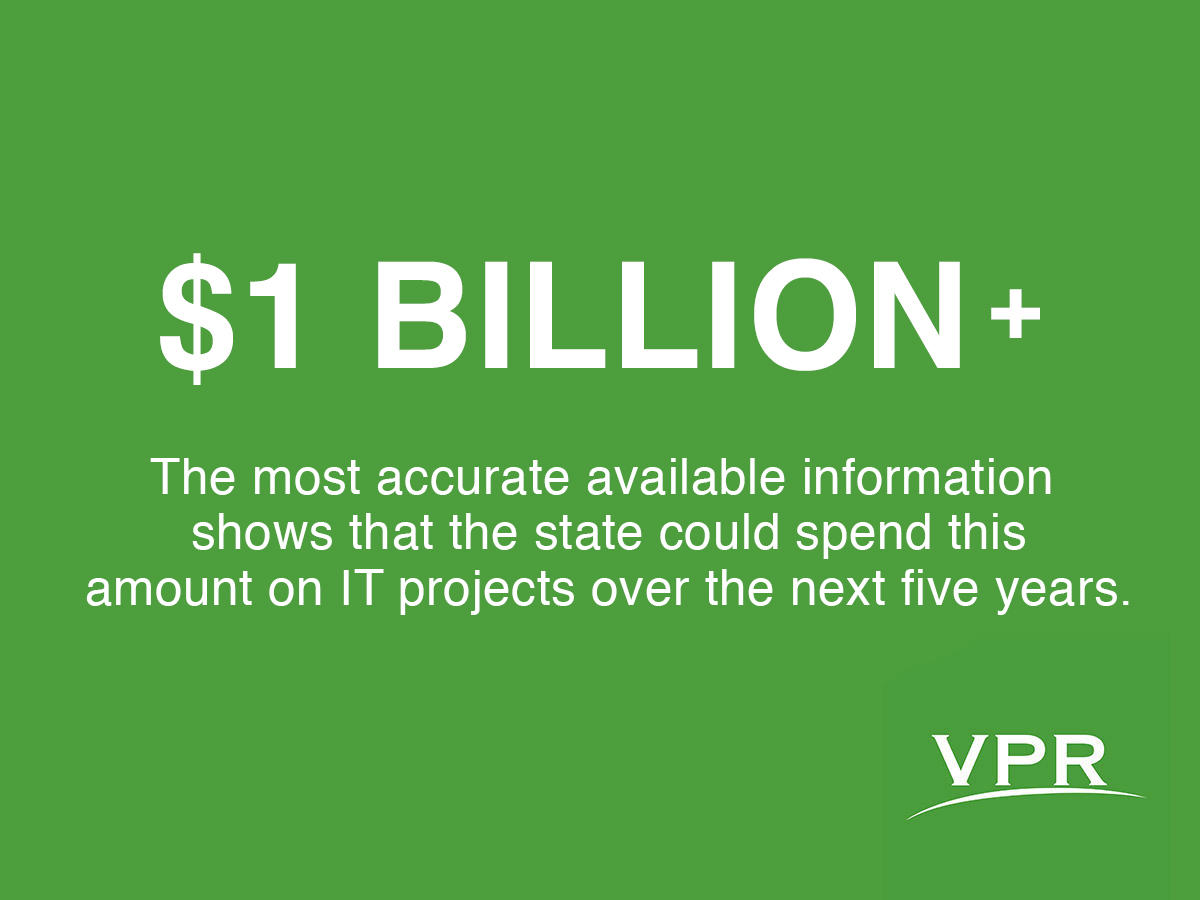

Delays and Debt Plague Vermont’s $1B+ IT Upgrades

Backlog of IT upgrades reaches $1 billion as state pays off obsolete technology. (Vermont Public Radio)

Backlog of IT upgrades reaches $1 billion as state pays off obsolete technology. (Vermont Public Radio)

The state of Vermont doesn’t track what it spends on information technology, so we did it ourselves.

As the Vermont Legislature works to overcome a $100 million budget gap for fiscal year 2016, one of its largest fiscal liabilities remains outside the reach of the annual budget bill. The state gives up about $1 billion in tax breaks annually through policies that have remained largely unchanged in recent years, even as lawmakers struggle to balance budgets.

Unlike state spending, most of the tax breaks are permanent – unless they’re amended. They’re not voted up or down annually like the budget. But every two years, the state tallies how much money it’s not collecting. Here’s the latest glimpse of who gets to keep it.